A pioneer in sustainable technology, Bennamann chose the World Biogas Expo 2025 to launch onto…

Putting AD on the Pathway to Zero Subsidy?

You may have noticed the headline for our Research and Innovation Forum this year is “Putting AD on the Pathway to Zero Subsidy”.

Of course government has been asking us as an industry for many years when we will match the cost reductions that solar and offshore wind have reached in the last decade or so. We know that AD is different, with a whole range of considerations that other technologies may not need to factor-in, such as feedstock and digestate management risks.

That is why two years ago ADBA set up an industry-led Cost Competitiveness Task Force, which concluded that with the right policy, new food waste AD projects could match the levelised cost of Hinckley Point C power plant by the time it was built. But Hinckley is subsidised.

Going further, to the point where AD receives no subsidy at all, would of course be helped by proper carbon pricing or some equivalent measure to penalise the fossil fuel competitor technologies. This carbon pricing would need to involve methane emission pricing from sources such as manure management. Fossil heating fuels would also need to be included.

Assuming carbon pricing doesn't progress, what other options do we have as an industry?

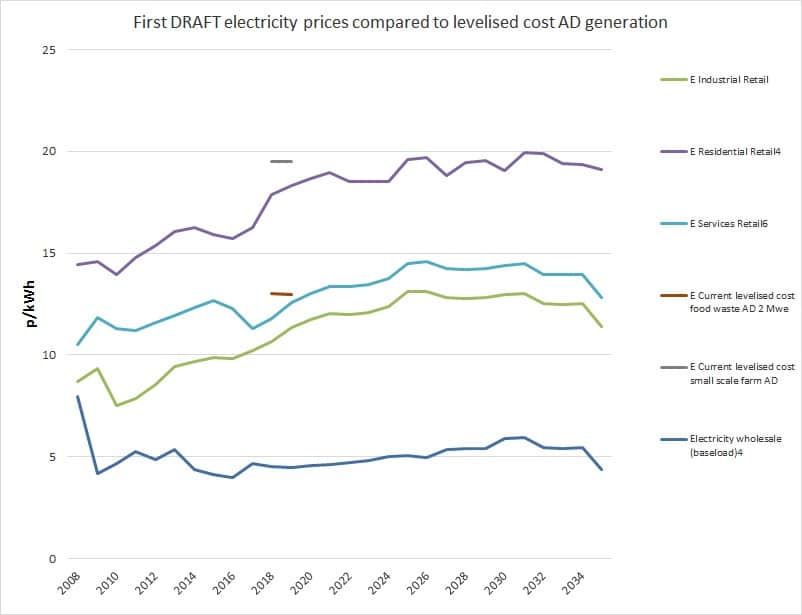

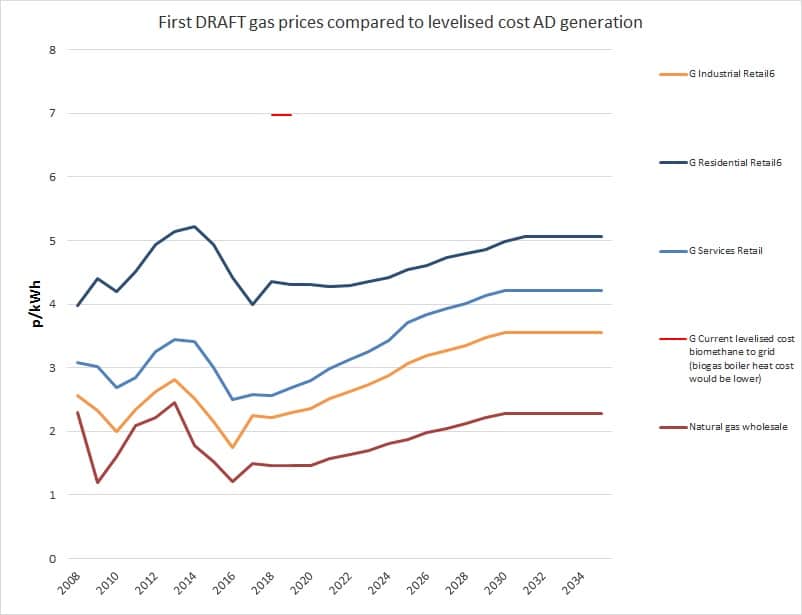

As can be seen from the below charts, the levelised cost of generating energy from AD (calculated simply using tariffs plus adding wholesale income) is significantly higher than both the wholesale prices AD plants can aim to reach, or the retail prices that customers are paying (which factor in transmission costs and the types of subsidy Hinckley and AD plants receive):

In the coming year we will be asking Treasury for more money for renewable gas, and we will not get a foot in the door unless we can set a glide-path towards new plants being built without subsidy.

So how, in the absence of carbon pricing, do we bridge this gap?

We've outlined in the past five areas that would help:

1. Committed government action on bringing more food waste into AD

2. Increased public and business awareness of AD

3. Investment in research and innovation

4. Recognition of benefits and use of digestate

5. Policy certainty and predictability in future tariff rates

It is the third of these points that as an industry we are in most control of: research and innovation.

Our industry is reliant on building industry-academic partnership that will deliver breakthrough processes and technologies like the research that got food waste AD up and running in the UK in the first place, including on which trace elements are most effective at boosting and stabilising food waste digestion.

And this R&I Forum programme covers many of the topics that will help set us on that path, including perspectives on maximising the efficiency of biogas use, improved crop growing techniques, speeding up and stabilising the digestion process, assessing how AD fits into the food-water-energy nexus, and the role of digestible packaging in the food supply chain.

I hope it will be a further step to us closing that gap.