MEMBER PRESS RELEASE - Biomethane developers file 38 applications for new or expanded UK plants in first…

MEMBER GUEST BLOG – Aligning Food Waste Recycling Policy with Biomethane Ambitions: A National AD Operator’s Perspective

MEMBER GUEST BLOG

Aligning Food Waste Recycling Policy with Biomethane Ambitions: A National AD Operator’s Perspective

By Luke Ford, Commercial Director, Biogen

Biogen own and operate 19 anaerobic digestion (AD) facilities across the UK; 12 food waste sites and 7 sites processing a combination of agricultural crops and non ABP residues. Biogen works with over 40 Local Authorities across the United Kingdom.

From an operator perspective, Simpler Recycling, whilst obviously welcome, has been plagued by two main problems:

Firstly, the delay to mandatory food waste collections for numerous years in England resulted in a significant over capacity of food waste treatment. This meant prolonged periods where unlucky sites operated below capacity and the lucky ones ran at a deviation to their investment cases to prop up significantly negative gate fees which ironically financially incentivised production of food waste. Operators helpless as investment flowed up the supply chain to brokers, waste handlers and producers.

Secondly, the uncertainty around food waste volumes combined with regulatory uncertainty over the future of the Green Gas Support Scheme (GGSS) has meant it is impossible to forecast volumes; effectively waste volume and treatment capacity won’t align. Uncertainty over enforcement of Simpler Recycling for businesses; announcements on transitional arrangements, allowance of co-mingling food and green waste and now the delays has meant it’s never been clear to our sector what the waste flows will look like in terms of either volume or location. Had more certainty been provided well in advance, it is far more likely procurement would have been earlier and investment would have been made to accommodate the influxes; sites would have been expanded and new sites built.

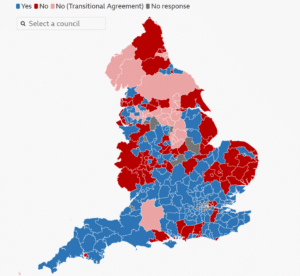

On the BBC website, there is a map of councils with three categories:

- those that will be rolling out on time (blue),

- those that will miss the deadline (red) and

- those that have a “transitional arrangement” (pink).

It’s easy to look at the map and see the big swathes of pink and red from the Midlands up and spreading across the North and feel that this is a sorry reflection of the North/South investment and opportunity divide, and to conclude that this may be more funding-orientated than contractual. If we explore the underlying factors of many of those councils in the “red” category it is fair to sympathise with some of their positions; unclear funding allocation, a national scramble to procure the correct vehicles and caddies, amendments to existing transfer networks all coinciding with a wider government programme of decentralising local authorities at a critical time.

It’s easy to look at the map and see the big swathes of pink and red from the Midlands up and spreading across the North and feel that this is a sorry reflection of the North/South investment and opportunity divide, and to conclude that this may be more funding-orientated than contractual. If we explore the underlying factors of many of those councils in the “red” category it is fair to sympathise with some of their positions; unclear funding allocation, a national scramble to procure the correct vehicles and caddies, amendments to existing transfer networks all coinciding with a wider government programme of decentralising local authorities at a critical time.

Transitional arrangements are a separate issue. There is only one transitional agreement in place South of Nottinghamshire which appears to only be until next year; does this mean that there are no long-term residual waste contracts in the South of the country? Or does it mean that those councils are committed to achieving higher recycling rates and will work with their contractors to backfill the capacity with alternate feedstock? Why have transitional arrangements, some as far out as 2043, been handed out so freely? Has the actual feasibility been assessed; reduced food stream and associated gate fee, backfill of commercial feedstock etc. or is it easier to just say “we have a contract, we’re not doing it”?

The map is a clear representation of current and future fracture of waste flows; it’s also only now that we have that map that the realisation is that some areas will be saturated with food waste whilst other areas are completely deprived and the infrastructure to transfer and bulk the waste across the country doesn’t really exist. Our view is that the Local Authorities aren’t the ones who will be affected as the majority have procured binding commitments; where is the local waste company running a dust cart service going to tip their food when the AD plant they run to is full of household waste and shuts their doors? If we see food waste going to landfill whilst some plants don’t have enough feedstock then we will inevitably be asking the question whether Simpler Recycling was implemented well.

As a sector, AD is central to so much progressive development; scaling up biomethane is central to decarbonisation of the gas grid but will also play a key role in the future of HGV and aviation fuel whilst also being the most efficient pathway for carbon dioxide removal. Given the ambitious UK targets for installed biomethane capacity (64TWH by 2050 NESO 2025 FES) compounded with the role biogas will play in adherence to RTFO and the SAF mandate the scale needs to be significant and therefore liberating food waste from residual waste streams is vital. As we move towards a commercial model that incentivises low carbon intensity scoring, several hundred thousand tonnes per annum of the best feedstock we can valorise not making its way to AD sites for many years is a wasted opportunity particularly when the main alternative is incineration.

AD is a sector where senior teams are dominated by project developers, renewables execs, finance specialists and regulatory experts; we may need to consider whether we are doing enough to champion the role of AD as a waste-treatment methodology and emphasise why it is so important that the feedstock reaches us? Do the resourcers need to be more vocal?

We stand by and don’t pass comment whilst blue chip retailers vandalise their supply chains by setting up inefficient segregation and backhauling procedures to separate bread and produce from food waste to then re-haul all streams from all distribution centres the length and breadth of the country on low payloads to a single processing location, to then reload once more to send the output to farms as animal feed all to claim waste “avoidance”. Due to our position on the waste hierarchy, manufacturers have similar mindsets and the obsession with black soldier fly bioconversion for similar reasons, despite a DEFRA commissioned life cycle assessment disproving its benefits, begs the question whether, with all AD has to offer, the food waste hierarchy should be reviewed and reconsidered. What we do, and have the potential to do, is so fantastic that the outward perception should be viewed as more than just “recycling” in the same way as composting is or “energy generation”.

Coming back to Simpler Recycling I’m sure all operators are welcoming the influxes of volumes and generally it will be heralded as a success as “recycling” rates improve nationally but the bigger question of a nationwide operator is; “if the value and potential of our sector was more widely understood would it have been handled differently?”